Trust Administration Series: Part 2 of 3

In Part 1 of 3 of this Trust Administration Series, we covered the trustee’s duties, liabilities, and trust administration checklist. Next, we will discuss the common subtrust structures of a family trust after the death of the first spouse to die.

Breaking Down the Subtrust Structure

The family trust is often divided into subtrusts upon the death of the first spouse to die for tax savings and asset protection purposes. Additionally, for the same reasons, they may be created for the benefit of the spouses’ children and more remote descendants on the death of the surviving spouse.

A brief overview of the subtrusts that may be created under the family trust is provided below. Following the death of the first spouse to die, the family trust is generally divided into the following common subtrust structures:

(1) AD Trust

(2) AB Trust

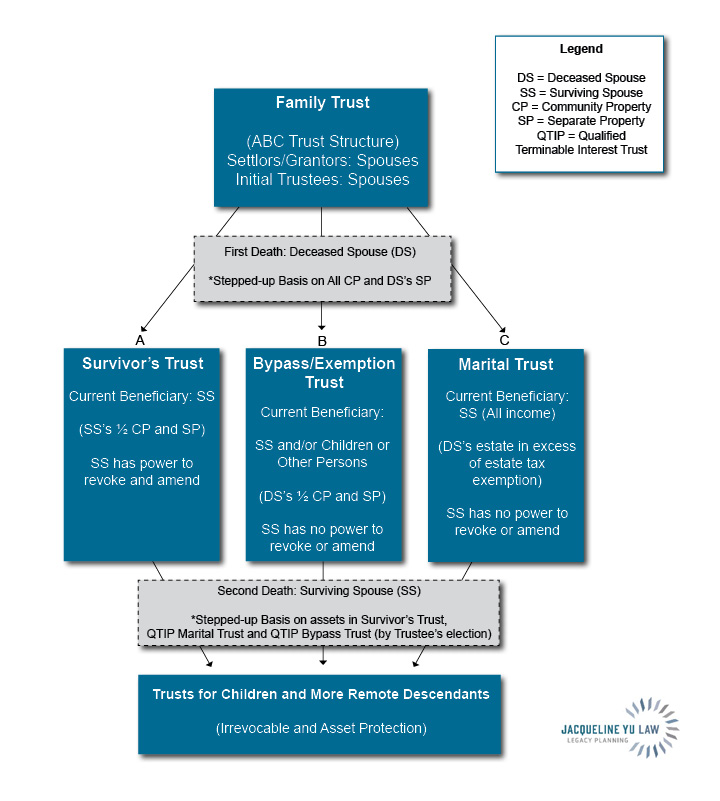

(3) ABC Trust

Survivor’s Trust

The Survivor’s Trust (sometimes called the “A Trust”) is a common term for the subtrust that is established following the death of the first spouse to die (the “deceased spouse”). This subtrust receives the surviving spouse’s interest in the trust estate (i.e., the surviving spouse’s one-half share of the community property and the surviving spouse’s separate property (if any)), and in some occasions, the deceased spouse’s interest in the trust estate as in the AD Trust structure (Survivor’s Trust with optional Disclaimer Trust) or the deceased spouse’s interest in the trust estate in excess of his or her available estate tax exemption as in the AB Trust structure. Any assets remaining in the Survivor’s Trust on the surviving spouse’s death will be included in the surviving spouse’s estate and receive a stepped-up basis for income tax purposes equal to the fair market value of the asset as of the surviving spouse’s death. The stepped-up basis would significantly minimize the capital gains tax consequences following the surviving spouse’s death if the children were to decide to sell the assets.

On the other hand, the Survivor’s Trust remains revocable and amendable by the surviving spouse during the surviving spouse’s lifetime, and the surviving spouse has complete power to deplete the assets of the Survivor’s Trust and gift these assets to whomever he or she wishes. Accordingly, the preservation of these assets in the Survivor’s Trust may be at risk for the interest of the remainder beneficiaries (i.e., the spouses’ children) if, for instance, the surviving spouse remarries.

Disclaimer Trust

The Disclaimer Trust, which is used in an AD Trust structure (Survivor’s Trust and Disclaimer Trust), is commonly used to provide flexibility in a structure in which the deceased spouse’s interest in the trust estate will continue to be held in a single-revocable trust after the first death, such as a Survivor’s Trust. The disclaimer trust provision gives the surviving spouse the option to minimize his or her future estate that may be subject to estate tax by disclaiming a portion or all of the deceased spouse’s interest in the trust estate within nine months from the deceased spouse’s date of death, and such disclaimed interest would then pass to an irrevocable trust to absorb all or part of the deceased spouse’s applicable estate tax exemption amount.

The surviving spouse must have no special power of appointment over the Disclaimer Trust, and if the surviving spouse is a trustee, he or she may not have the power to direct the distribution of the income to other beneficiaries. The value of the disclaimed interest and any future appreciation thereon would be excluded from the surviving spouse’s estate. The Disclaimer Trust is irrevocable and may not be amended or revoked by the surviving spouse, and accordingly, provides some level of preservation of the principal of the assets in the Disclaimer Trust for the benefit of the remainder beneficiaries. On the other hand, because the assets of the Disclaimer Trust are excluded from the surviving spouse’s estate, these assets will not receive stepped-up basis on the surviving spouse’s death.

Bypass Trust

While the Disclaimer Trust is created on an as needed basis by the surviving spouse’s election following the deceased spouse’s death, the Bypass Trust (sometimes called the “B Trust,” “Credit Trust”, “Exemption Trust”, “Decedent’s Trust,” “Residuary Trust” or “Credit Shelter Trust”) is written into the trust agreement to be established upon the death of the deceased spouse. The Bypass Trust is part of the common AB Trust structure (Survivor’s Trust-Bypass Trust). The Bypass Trust is designed to hold the deceased spouse’s interest in the trust estate, which comprises the deceased spouse’s one-half share of the community property and separate property (if any) up to the amount equal to the deceased spouse’s available estate tax exemption as of date of death.

Similar to the Disclaimer Trust, the Bypass Trust is irrevocable and may not be amended or revoked by the surviving spouse. Accordingly, the Bypass Trust provides a level of preservation of its assets for the benefit of the remainder beneficiaries. On the other hand, because the assets of the Bypass Trust are excluded from the surviving spouse’s estate, these assets will not receive stepped-up basis on the surviving spouse’s death. The Bypass Trust may be structured as a hybrid trust known as a QTIPable Bypass Trust that allows a Qualified Terminable Interest Trust (QTIP) election (as further discussed below) for a portion of the deceased spouse’s share of the trust estate so that stepped-up basis may be achieved for these assets on the surviving spouse’s death while preserving these assets during the surviving spouse’s lifetime.

Marital Trust

The Marital Trust (sometimes called the “C Trust,” “QTIP Trust,” or “Marital Deduction Trust”) is part of the common ABC Trust structure and is generally designed to qualify for the marital deduction and hold a portion of the deceased spouse’s interest in the trust estate that is equal to the value of the deceased spouse’s estate that is in excess of his or her estate tax exemption amount. The function of the Marital Trust is to avoid the estate tax on the death of the deceased spouse while preserving the assets of the Marital Trust during the surviving spouse’s lifetime because of its irrevocability. To qualify the assets in the Marital Trust for the marital deduction and avoid the estate tax on the deceased spouse’s death, the trustee must make a QTIP election on the deceased spouse’s estate tax return, and the dispositive provisions of the Marital Trust must provide that:

(1) The surviving spouse must be entitled to all the income from the property, payable at least annually, or have an interest for life in the property

(2) No person, including the surviving spouse, may have a power to appoint any part of the Marital Trust assets to any person other than the surviving spouse unless the power of appointment is a testamentary power of appointment

The Marital Trust may not be revoked or amended by the surviving spouse; but its assets will be included in the surviving spouse’s gross estate and accordingly will receive stepped-up basis on the second death. As discussed above, a QTIP election may also be made for a portion of the assets of the Bypass Trust to receive stepped-up basis on the surviving spouse’s death. To qualify for the QTIP election for the Bypass Trust assets, it must be made on the deceased spouse’s estate tax return, and the dispositive provisions listed above must also be provided for the terms of the Bypass Trust under the trust agreement.

Subtrusts for Children and More Remote Descendants. Once the surviving spouse dies, often the remaining balance of the family trust is distributed either outright or in further lifetime trusts for the benefit of the spouses’ children, grandchildren, and more remote descendants, thereby allowing a tax efficient method of achieving intergenerational transfers of wealth.

See Article: Use It or Lose It: It’s Time to Maximize on Your Estate and Gift Tax Exemption

ABC Trust Structure

*Creating lifetime subtrusts for the benefit of children, grandchildren, and more remote descendants serve as vehicles for intergenerational transfers of wealth that are free of estate tax and generation-skipping transfer (GST) tax if the trustee allocates sufficient estate tax exemption and GST tax exemption from the Deceased Spouse and Surviving Spouse on timely filed estate tax returns. Note: GST tax is separate from, and in addition to, the estate tax, and is imposed on transfers of assets to beneficiaries who are either (1) unrelated to the settlors/grantors and 37 ½ years younger than the settlors/grantors or (2) related to the settlors/grantors and more than one generation younger than the settlors/grantors (i.e., grandchildren and more remote descendants). The GST tax is a flat 40% tax on the value of assets transferred in excess of the GST tax exemption. Currently, the estate tax exemption is $12.06M per spouse and the GST tax exemption is $12.06M per spouse.

Contact Jacqueline Yu to discuss the administration of your subtrusts by sending an email to info@jacquelineyulaw.com or calling 310-313-1195.

Related posts

Corporate Transparency Act Alert

Read more about Corporate Transparency Act Alert