When Proposition 19 passed in the November 2020 election, many voters did not fully understand the long-term implications of the new law. This change greatly impacts the intergenerational families that make up so much of the fabric of California. It affects families who have moved or immigrated to the state (the population of California is one-third foreign-born), built their wealth in real estate, and want to pass it on to the next generation. Now, children who inherit property from their family face the possibility of property tax reassessment, something that can amount to a large financial burden. That is the last thing that parents or grandparents want to pass onto their families.

In the ATTOM Data Solutions’ Year-End 2018 U.S. Home Equity & Underwater Report, California had the highest number of equity-rich homeowners in the U.S., at 43.6%. The company defines equity-rich homes as those where the value of the home is 50% or more than the total loan amount.

Homeowners in California who desire to keep their real estate in the family, need to understand the new rules under Proposition 19. We will help you navigate your future real estate succession planning and provide a sound estate planning strategy for avoiding costly property tax reassessment.

California’s Proposition 19 and Property Tax Reassessment

Proposition 19 eliminates a parent’s ability to leave their children or grandchildren their Proposition 13 taxes and tax base. Nearly all property will be reassessed at its current fair market value—with one very small exception which we will discuss in a moment. It is important to know that Proposition 19 effectively eliminated Proposition 58, which allowed for unlimited property tax reassessment exclusion for transfers of primary residences between parents and children or grandparents and grandchildren.

Whenever there is a change in ownership of real property, a property tax reassessment occurs. In California, there are two situations and resulting rules around reassessment:

- You directly own the property

- You own property through an entity such as an LLC, partnership, or corporation

The first situation is what Proposition 19 directly affects: transferring direct ownership of real property by lifetime or testamentary gift (inheritance), or a sale deemed a “change in ownership” that would trigger a property tax reassessment. The property’s full reassessment will be based on the property’s fair market value upon the date of the transfer (or change of ownership). How could this become a problem? Real estate in California continues to skyrocket in value and when a property is reassessed at the higher current fair market value than the prior property tax base, the new owner now has to pay higher property taxes, which can be in the high-five-figure range.

There are limitations on reassessment still in place under Proposition 13. Proposition 13 provides an established base year value, a restricted rate of increase on assessments of no greater than 2% per year, and a cap on property taxes to 1% of the assessed value (plus voter-approved local and county taxes, if applicable). While these limitations exist, a 2% increase in property taxes in a given year could still be a large amount, depending on the property.

Now, back to the exception within Proposition 19. The only reassessment exclusion available for transfers of property between parents and children or grandparents and grandchildren is a transfer of principal residence so long as:

- The child moves into the transferred or inherited property as the child’s principal residence within one year of the transfer and,

- The property is worth less than the total of the property’s base year value plus $1M.

Yes, you read that correctly, the child would have to move into the property and make it their primary residence. How often does that actually happen? Rarely. By now the children are adults, probably have a home of their own, and likely want to use the residence as a vacation home or a rental. Additionally, under Proposition 19, the transfer of secondary residences is no longer available as an exclusion.

Considering these restrictions, we have a strategy that adds another layer of planning to help you avoid property tax reassessment when you are ready to pass real estate to your loved ones.

A Long-Term Strategy for Gifting Real Estate Without Property Tax Reassessment

Even under Proposition 19, there is no reassessment for a transfer of 50% or less of ownership in a real estate holding. For this reason, parents can transfer real property to their children without reassessment if the real property is owned by an LLC, partnership, or corporation. The transfer of the interest in the entity must be 50% or less of the ownership in the entity. So long as no one person ends up with more than 50% ownership in the real estate holding or ends up with control, there is no reassessment.

Below is a strategy that is the best situation for families that do not intend to sell their real estate for a long time. It is one that is appropriate for children who intend to keep the real estate for their long-term investment and pass on the family inheritance to their descendants.

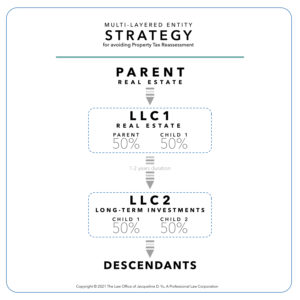

A Multi-Layered Entity Strategy for Avoiding Property Tax Reassessment

It is key to understand that ownership of real estate within an entity such as an LLC has a different set of rules. It is only a change in ownership if you transfer a majority interest in that entity to someone else. Majority interest is 51% and above, and a transfer of a majority interest in the entity would trigger a property tax reassessment. But if you transfer 50% or less of your ownership interest in the entity, no reassessment occurs.

In our example strategy, a mother has two children. In the first step of the strategy, she transfers the entire property into an LLC, in which she is the sole member of the LLC (LLC1 for this purpose). There is no change in ownership because the prior owner of the property is also the sole member of the LLC. The mother then transfers 50% of LLC1 to child 1. No property tax reassessment occurs because the interest transferred in LLC1 is not a transfer of a majority interest.

Now, the mother and child 1 need to hold onto that property in LLC1 for at least one year; two years is best. This allows enough time in between transfers so that the series of transfers are not treated as a single transaction that would trigger a reassessment.

The mother and child 1 then take the property out of LLC1 and hold the property in their individual names as co-owners. There is no change in ownership because the transfer changes only the manner in which title is held in the property and the mother and child 1 hold the same proportional interest in the property before and after the transfer.

Next, the mother and child 1 create a new LLC (LLC2) and transfer the property into LLC2, in which the mother and child 1 each own a 50% interest in LLC2. Again, no reassessment occurs because the transfer changes only the manner in which title is held in the property, and the mother and child 1, as original co-owners of the property, hold the same proportional interest in the property before and after the transfer. They wait another year at a minimum.

Finally, the mother transfers 50% of LLC2 to child 2. Once again, there is no reassessment due to there not being a transfer of a majority interest in LLC2. The end result is that child 1 now owns 50% of LLC2; child 2 owns 50% of LLC2; and the mother is out of the equation, while avoiding property tax reassessment. The children are free to pass each of their 50% interest in the real estate holding to their descendants eventually.

Plan Now, for Long-Term Real Estate Succession

When executed correctly, this long-term, ongoing strategy ensures that the property will not be reassessed upon gifting the property to subsequent generation(s). Proposition 19 greatly affects the middle class and the intergenerational families of California that have built their wealth in real estate and want it to stay in their family for many generations to come. If you plan to gift your real estate to your children or grandchildren, start planning now to avoid leaving them with a large property tax burden. In addition to property tax, if you would like to learn more about other intergenerational transfer strategies to minimize your estate, gift and generation-skipping transfer tax burden, contact Jacqueline Yu at info@jacquelineyulaw.com or 310-313-1195.

Related posts

Corporate Transparency Act Alert

Read more about Corporate Transparency Act Alert