As parents age, they begin to think about estate planning, and they naturally want to pass on their assets in the most efficient, and least tax-burdensome manner. Two very important factors to consider in estate planning are asset protection and estate tax exemption. There is a trust that spouses can establish for the benefit of each other that provides asset protection for both of them, preserves their estate tax exemptions, and offers continued access to the trust’s funds. This trust is called the Spousal Lifetime Access Trust (“SLAT”).

We will discuss how to create a SLAT and provide asset protection for yourself, and your family, while maximizing on your estate tax exemption.

What is a Spousal Lifetime Access Trust?

A Spousal Lifetime Access Trust is a lifetime gift from one spouse (the “grantor spouse”) to an irrevocable trust for the benefit of the other spouse (the “beneficiary spouse”) during the beneficiary spouse’s lifetime. A SLAT is funded by gift while both spouses are alive.

The gift to the SLAT will be covered by the grantor spouse’s applicable estate tax amount, removing all the assets in the trust and any appreciation thereon outside of the grantor spouse’s and beneficiary spouse’s estates, thereby reducing the exposure of both spouses’ estates to the estate tax, while shielding these assets from the creditors of both the grantor spouse and the beneficiary spouse. It is the appreciation on the assets transferred to the SLAT that truly escapes federal estate tax. Moreover, since the grantor and beneficiary are married, the grantor spouse will continue to have access to the funds indirectly through the beneficiary spouse during his or her lifetime.

SLAT estate planning is an attractive option for married couples who are not ready yet to distribute their wealth to their children and need access to the trust’s assets but want to maximize on their estate tax exemption and provide asset protection for their family’s wealth.

Three Challenges, One Solution Within a SLAT

A SLAT effectively addresses three issues:

1. Asset Protection. The assets held in a SLAT are protected from the claims of creditors of both the grantor spouse and the beneficiary spouse. On the beneficiary spouse’s death, if the assets continue to be held in trust for the benefit of the spouses’ children, grandchildren and more remote descendants, these assets are protected from the claims of creditors of the beneficiary descendant and from the reach of a beneficiary descendant’s spouse in the event of a divorce. Note, however, that any distributions made to the beneficiary spouse for beneficiary descendant from the SLAT would be within creditors’ reach. So long as assets remain in the SLAT, they are shielded from creditors’ claims.

2. Preserve Your Gift, Estate, and GST Tax Exemption Amount. Individuals may transfer (either during their lifetime or at death) up to the gift and estate tax exemption amount (currently, $11.7 million per individual) free from federal gift and/or estate tax. This is a unified exemption amount such that if the entire $11.7 million exemption was used during an individual’s lifetime, then such individual would have exhausted his or her exemption for transfers upon death. Transfers over the gift and estate tax amount are subject to a 40% tax. By having each spouse create a SLAT, each spouse can preserve their respective maximum current gift and estate tax exemption before the exemption will be significantly reduced at its scheduled sunset on January 1, 2026 (or earlier if a reduction in the exemption becomes effective under President Biden’s tax plan).

In addition to the gift tax (lifetime gifts) and estate tax (testamentary gifts), there is also the generation-skipping transfer (GST) tax. This is a separate tax that applies (either during lifetime or at death) to gifts to individuals who are two or more generations below you (e.g., a grandchild or great grandchild) or who are at least 37.5 years younger than you. The idea around the GST tax is to ensure that taxpayers don’t try to skip a generation to avoid a layer of estate tax. The GST tax exemption is the same as the gift and estate tax exemption, which is $11.7 million. The grantor spouse can allocate his or her additional GST tax exemption to the SLAT, making the transfer of wealth to his or her grandchildren, great grandchildren, and more remote descendants exempt from gift and estate tax for many generations.

3. Access to Trust Funds. The Trustee of the SLAT can make distributions to the beneficiary spouse on an absolutely discretionary basis, or subject to an ascertainable standard of health, education, maintenance and support (“HEMS”). The beneficiary spouse can act as a trustee of the SLAT but the beneficiary spouse’s power to make distributions to himself and herself must be limited by a HEMS standard. Any distributions that are made for purposes beyond the HEMS standard must be exercised by a third-party, independent trustee so that the assets of the SLAT continue to be excluded from the beneficiary spouse’s estate and protected from creditor’s claims. The same rules apply when the SLAT continues for the benefit of a beneficiary descendant, who is acting as trustee. During the beneficiary spouse’s lifetime, the grantor spouse continues to have indirect access to the SLAT’s assets by virtue of his or her marriage to the beneficiary spouse.

The Benefits of an Irrevocable Trust

A SLAT is an irrevocable trust vehicle. To understand why a SLAT is unique, it is helpful to go over the difference between revocable and irrevocable trusts.

A trust is a relationship in which a person (commonly referred to as the “grantor”) gives property to another person or entity (the “trustee”) to manage that property for the benefit of the individual who is named as a beneficiary of the trust.

There are two broad categories of trusts: Revocable Trusts and Irrevocable Trusts.

Revocable Trust

A revocable trust is one that can be amended or revoked by the grantor at any time. On revocation, the trust assets revert to the grantor. Think of this type of trust like your alter ego. It is associated with your social security number, and it is an extension of yourself. A revocable trust provides no asset protection. Creditors can pierce through that trust to access the assets because you completely own those assets. What a revocable trust has going for it is that it allows you to avoid probate. This means there will be no public court proceedings to administer and distribute the assets of your estate. The absence of court fees is a plus for some, as is avoiding public disclosure of your estate.

Irrevocable Trust

An irrevocable trust is one that cannot be revoked or amended by the grantor. It is a separate entity, and it oftentimes has a separate taxpayer identification number. In order to exclude the assets of an irrevocable trust from the beneficiary’s estate and maintain a layer of asset protection for the beneficiary, the power to make distributions from the trust must be limited by a HEMS ascertainable standard if a beneficiary is acting as a trustee of the trust, and any discretionary distributions for purposes beyond the HEMS standard must be exercised by a third-party, independent, non-beneficiary trustee.

The creator of the trust, the grantor, cannot be a trustee of the irrevocable trust to maintain the exclusion of the assets of the irrevocable trust from the grantor’s estate, and in California, the grantor cannot be named as a beneficiary of the irrevocable trust to maintain an asset protection shield for the assets transferred to the SLAT. In California, if the grantor of the irrevocable trust is also a named beneficiary of the trust (also known as a “self-settled” trust), the asset protection shield is destroyed. Creditors can reach the assets of a self-settled trust under California law. (Note that a revocable trust is a self-settled trust).

To achieve asset protection under California law when you would like to continue to have some access to the assets, you can create an irrevocable trust, and instead of naming yourself as the beneficiary, name your spouse. By naming your spouse as the lifetime beneficiary, you have indirect access to the assets of the irrevocable trust during your spouse’s lifetime. And by putting your assets into an irrevocable trust for the benefit of someone else and giving up control of those assets, they are no longer considered yours in cases of bankruptcy or litigation. You can then realize the benefits of a SLAT.

However, it is important to keep in mind that your indirect access to the assets of the SLAT terminates upon your beneficiary spouse’s death. Accordingly, when thinking about creating a SLAT, assets that will be needed to support your lifestyle should not be transferred to the trust.

Maximizing Your Gift, Estate, and GST Tax Exemption

The 2017 Tax Cuts and Jobs Act (“TCJA”) significantly increased the federal gift, estate, and GST tax exemption from a $5.49 million exemption amount pre-TCJA to currently an $11.7 million exemption amount after the enactment of TCJA. Today, a married couple can transfer approximately $23.4 million of their wealth without having to pay a gift, estate or GST tax. However, as previously mentioned, unless Congress takes further action, this exemption is scheduled to sunset to pre-TCJA exemption levels (indexed for inflation) on January 1, 2026. It is anticipated that the exemption amount will be reduced to $6 million per individual, after inflation adjustments, upon sunset.

On November 26, 2019, the Treasury Department and the Internal Revenue Service issued final regulations under IR-2019-189 confirming that taxpayers who take advantage of the increased gift and estate tax exemption will not be adversely impacted when TCJA sunsets. Accordingly, individuals planning to make large gifts before TCJA sunsets can do so without concern of a “clawback” – that they will lose the tax benefit of the higher exemption amount once it decreases after 2025.

As an example, assume an individual transfers $11.7 million into an irrevocable trust this year, and subsequently dies after January 1, 2026, when the estate and gift tax exclusion has reverted to an inflation-adjusted $6 million. The estate would not have to pay estate tax on the extra $5.7 million gift. Instead, the IRS rules provide that the full $11.7 million would be exempt from estate tax.

Read More on the Estate and Gift Tax Exemption: Use It or Lose It, It’s Time to Maximize on Your Estate and Gift Tax Exemption

Grantor Trust Status

For federal income tax purposes, the SLAT is treated as a “grantor trust.” This means that the grantor spouse is for income tax purposes treated as owning the assets of the SLAT but not for gift, estate and GST tax purposes. Transfers of assets to the SLAT are deemed completed gifts.

Grantor trust status means that the grantor spouse is responsible for paying the income tax on any income earned on the assets of the SLAT. Although the grantor spouse pays income tax on the income received by the SLAT (and not by the beneficiary spouse), this has the added benefit of allowing the value of the assets of the SLAT and their appreciation to compound without being reduced by income taxes.

Asset Protection Under California Law

Transferring assets to a SLAT may also provide a measure of protection from creditor claims on both the grantor spouse, the beneficiary spouse, and the spouses’ children, grandchildren and more remote descendants, who are the contingent beneficiaries upon the beneficiary spouse’s death. Assuming the transfer to the SLAT is not a fraudulent conveyance made in order to hinder or delay creditors of the grantor spouse, the transferred assets to the SLAT should be free from the claims of the grantor spouse’s creditors because the grantor spouse has parted with dominion and control over the transferred assets and has not retained any interest in the SLAT.

It is important to note the distinction between the types of asset protection trusts and how they are viewed under California law. A person can create their own irrevocable trust and name themselves beneficiary; this is called a self-settled trust. However, under California law, self-settled trusts do not provide asset protection. In other words, creditor protection is voided for self-settled trusts.

California law does allow for the creation of asset protection trusts for the benefit of third parties, such as the spouse or children of the grantor. SLATs, in which the grantor’s spouse is the named beneficiary, provide asset protection under California law (it is not a self-settled trust). At the same time, by virtue of the grantor’s marriage to the beneficiary spouse, the grantor may access the funds of the SLAT indirectly through the beneficiary spouse.

Under California law there are three common types of third-party asset protection trusts. These types of trusts preclude the grantor from directly accessing the trust’s beneficial interest.

- Spendthift Trusts. These trusts have a limitation on how the assets of an irrevocable trust can be transferred. The beneficiary of this trust cannot assign these assets to the beneficiary’s creditors or the beneficiary’s estate.

- Support Trusts. These trusts provide an ascertainable HEMS standard limiting distributions to the beneficiary for purposes of the beneficiary’s health, education, maintenance, and support.

- Discretionary Trusts. These trusts grant the trustee sole discretionary authority to make a distribution to the beneficiary. The trustee has the absolute discretion to determine whether to withhold distributions or make distributions for the benefit of the beneficiary.

If the beneficiary spouse is not a trustee of the SLAT, assuming that the terms of the SLAT include a proper spendthrift clause, preventing the assignment of the SLAT’s assets by its beneficiaries, and the beneficiary spouse has only a discretionary interest in the SLAT, the assets of the SLAT should also be exempt from the beneficiary spouse’s creditors. Discretionary interest means the beneficiary spouse will receive trust income or principal only in the absolute discretion of an independent trustee.

If the beneficiary spouse is a trustee of the SLAT, distributions should be mandatory or subject to a HEMS ascertainable standard. An independent, third-party, non-beneficiary trustee must exercise any power to make distributions beyond the HEMS ascertainable standard for the beneficiary spouse’s benefit in order to maintain the trust’s asset protection shield for the beneficiary spouse and to exclude the SLAT’s assets from the beneficiary spouse’s estate.

The same terms apply to any continued trusts under the SLAT for the benefit of your children, grandchildren and more remote descendants.

In sum, SLATs are a way of providing asset protection to both the grantor, the grantor’s spouse, and their descendants under California law as well as providing access to the assets of the SLATs to the grantor’s spouse directly, and the grantor indirectly.

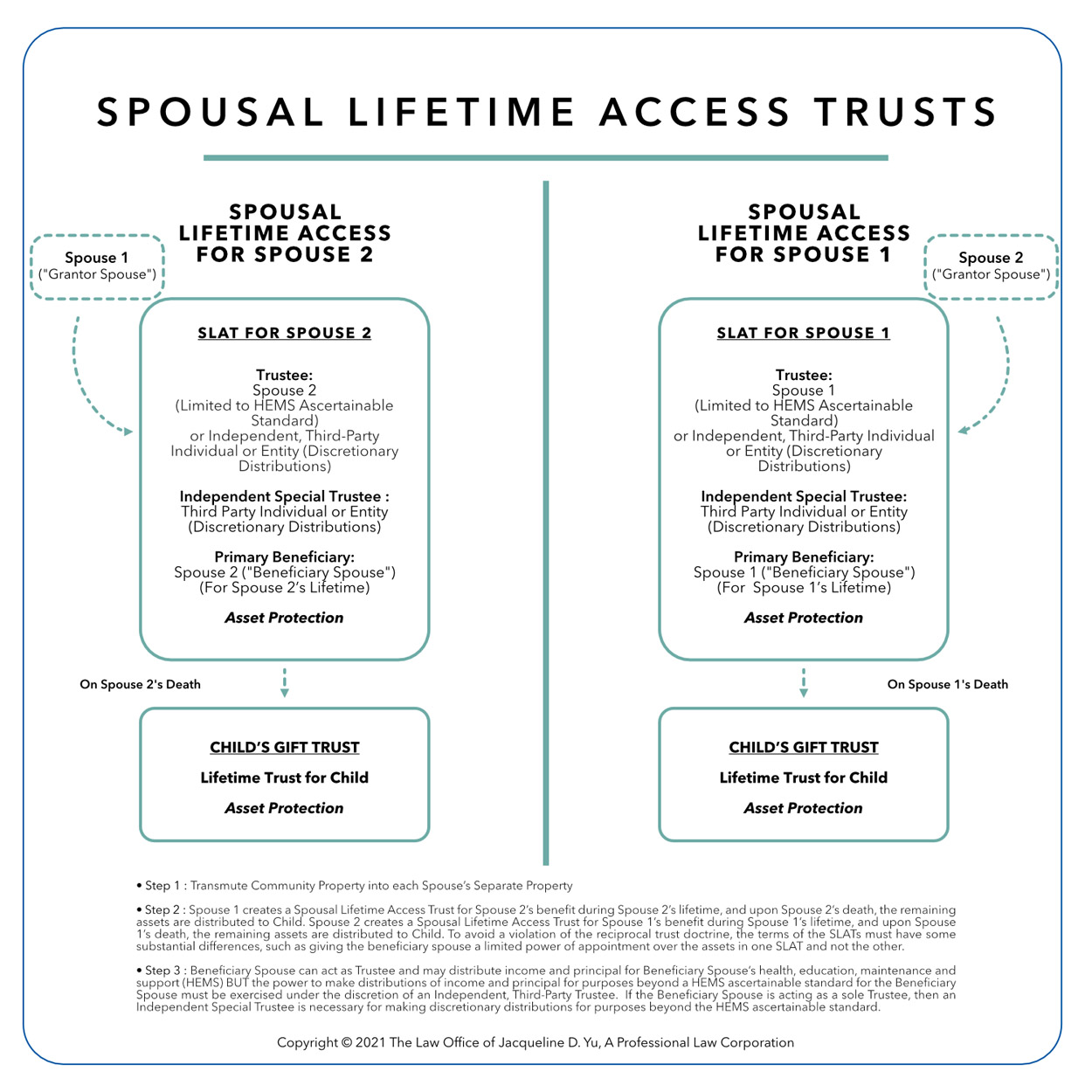

Creating Two SLATs Within a Marriage

It is possible to create two SLATs within a marriage. Each spouse can benefit indirectly from the SLAT created for the other’s benefit. There are key steps involved in this in order to set up two SLATs correctly.

Changing Community Property to Separate Property

First, before going into the trust, any assets the spouses own together as community property must be changed (or “transmuted”) to each spouse’s separate property. This is the only way you can apply your gift, estate and GST tax exemption to the assets transferred to the SLAT for your spouse’s benefit. Absent a transmutation of community property to a grantor spouse’s separate property before transferring these assets to the SLAT, the IRS would apply the unlimited marital deduction for these transfers instead of your gift and estate tax exemption.

Reciprocal Trust Doctrine

Second, you need to ensure that you do not run afoul of the IRS reciprocal trust doctrine. The reciprocal trust doctrine is designed to avoid abusive situations, such as where two spouses create identical SLATs for the other, seeking to avoid estate tax on the value of the trusts. Under IRS rules, if both spouses created a SLAT for each other, and if the SLATs have identical terms, the reciprocal trust doctrine allows the IRS to “uncross” the trusts, so that the grantor spouse is deemed to have created a trust for himself or herself (instead of the grantor’s spouse), thereby including the value of the assets transferred to the SLAT in the grantor spouse’s estate for estate tax purposes, ultimately defeating the estate tax exclusion purpose of the SLAT.

To avoid a violation of the reciprocal trust doctrine, the terms of the SLATs must have some substantial differences, such as giving the beneficiary spouse a limited power of appointment over the assets in one SLAT and not the other. Before that beneficiary spouse dies, they can exercise this limited power of appointment to choose which of their remaining beneficiaries inherit those assets.

Our chart explains the SLAT process for spouses (click to enlarge in new tab).

Why SLAT Estate Planning Could Become Very Important, Very Soon

Right now, everyone has an $11.7 million exemption. You can transfer assets to anyone, as long as it is below that amount, without estate tax, without gift tax, and without GST tax.

However, if President Biden’s tax plan goes into effect next year, which is likely, part of the proposal is reducing the exemption per individual to between $3.5 million to $6 million (adjusted for inflation). Even if the plan does not go into effect, the $11.7 million gift, estate and GST tax exemption is scheduled to sunset by January 1, 2026, to pre–Tax Cuts and Jobs Act levels. That would be approximately $6 million after inflation adjustments.

So, a SLAT can preserve the $11.7 million exemption that you currently have now, before it decreases and you lose out on that additional $5 million exemption that you could have used to minimize your wealth’s exposure to gift, estate and GST taxes.

When a SLAT is Right for a Married Couple

Every marital situation is unique and brings up different considerations. Wealth, age, blended marriages and/or children are all factors that come into play. There are many types of trusts, but SLATs are certainly an effective estate and tax planning tool.

For further information on SLAT estate planning and tax planning, contact The Law Offices of Jacqueline D. Yu at info@jacquelineyulaw.com and (310) 313-1195.

Related posts

Corporate Transparency Act Alert

Read more about Corporate Transparency Act Alert